What Is Bootstrapping in Business? How to Launch and Grow Using Only Your Own Resources

Have you ever dreamed of starting your own business but felt held back by the daunting prospect of securing funding? You’re not alone. Many aspiring entrepreneurs wrestle with this very concern, but what if I told you that you don’t necessarily need a suitcase full of cash or an army of investors to bring your vision to life? Welcome to the world of bootstrapping! In this article, we’ll explore what bootstrapping really is, how it empowers you to launch and grow your business using only your own resources, and why this approach might just be the secret ingredient to your entrepreneurial success. So, grab a cup of coffee, and let’s dive into the art of building a thriving business from the ground up—one smart decision at a time. Ready to take charge of your entrepreneurial journey? Let’s get started!

Understanding Bootstrapping and Its Importance in Business

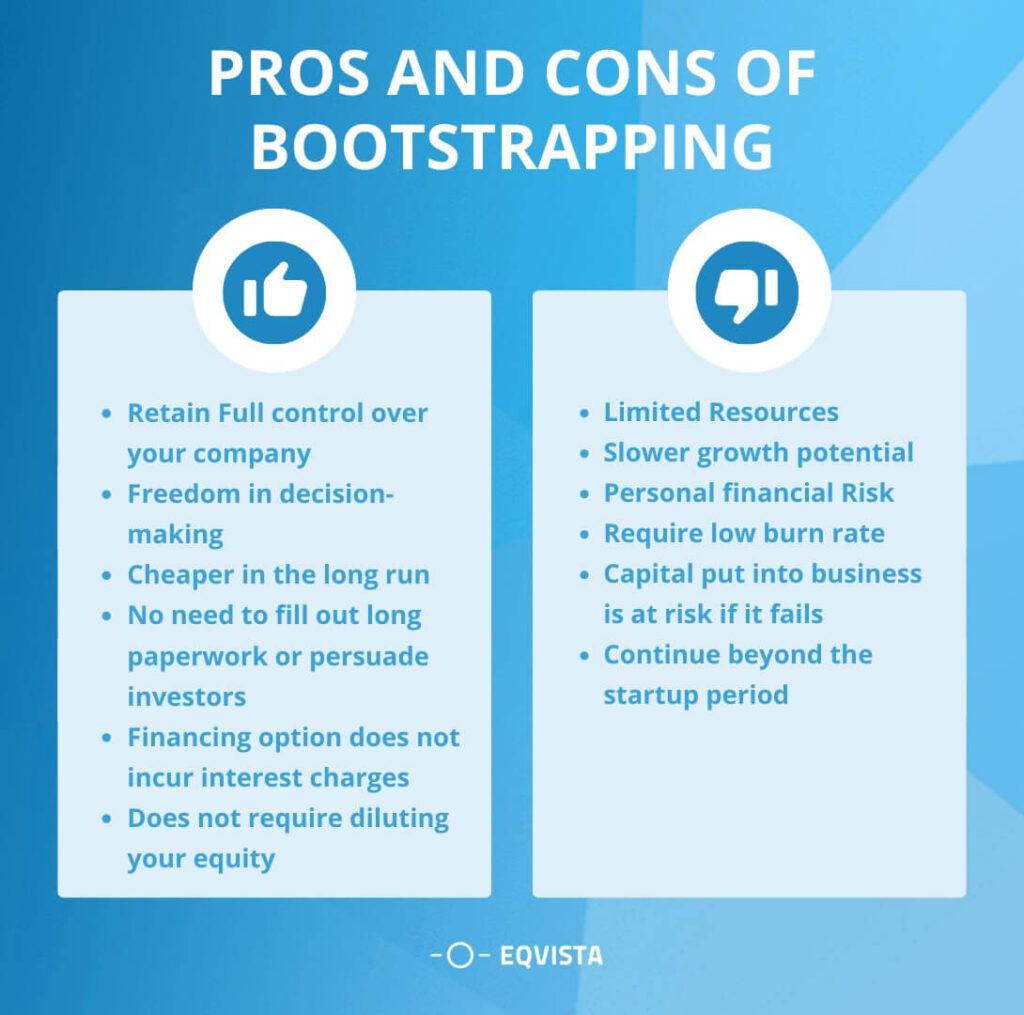

Bootstrapping refers to the practice of starting and growing a business with minimal external funding. Entrepreneurs often rely on personal savings, revenue generated from early sales, and innovative strategies to propel their ventures forward. This approach allows for greater control over the business and can foster a more resilient foundation for future growth. By focusing on efficiency and resourcefulness, bootstrapped businesses often develop a stronger connection with their customers and a clearer understanding of market needs.

One of the most significant advantages of bootstrapping is the ability to maintain full ownership and control of your company. When you avoid external funding sources, such as venture capital or angel investors, you retain the freedom to make decisions that align with your vision. This autonomy can be particularly empowering during the early stages of your venture, allowing you to pivot quickly based on feedback and market dynamics.

Additionally, bootstrapping encourages financial discipline. Entrepreneurs must carefully monitor expenses and prioritize investments that yield the most significant returns. As a result, many bootstrapped businesses become adept at operating lean, focusing on essential elements that drive growth. This practice often leads to a culture of innovation, as teams brainstorm creative solutions to overcome limitations.

Starting small and scaling gradually can also be a strategic advantage. By launching with a minimum viable product (MVP), you can test the waters without committing extensive resources. This approach allows you to gather valuable feedback, iterate on your offering, and build a loyal customer base before expanding your operations. It’s a smart way to validate your business model without the pressure of significant financial risk.

However, bootstrapping is not without its challenges. Limited resources can restrict your ability to market your product effectively or invest in talent. To combat this, consider leveraging strategic partnerships and networking opportunities that can amplify your reach without incurring substantial costs. Collaborating with other entrepreneurs or businesses can lead to mutually beneficial arrangements and shared resources.

It’s also essential to focus on customer relationships. Bootstrapped businesses can thrive by cultivating a loyal customer base through outstanding service and engagement. By establishing strong communication channels and prioritizing feedback, you can create a community that supports your growth. This grassroots approach often leads to authentic brand ambassadors who will advocate for your business through word-of-mouth.

bootstrapping offers a unique pathway to launch and scale a business. By leveraging your own resources, maintaining control, and fostering creativity, you can build a sustainable enterprise that resonates with your audience. While it may require more effort and dedication initially, the potential rewards of running a bootstrapped business often outweigh the challenges.

The Benefits of Bootstrapping: Why Relying on Yourself Matters

When it comes to launching a business, many entrepreneurs find themselves at a crossroads: seek external funding or bootstrap the venture using their own resources. The latter approach, while often seen as risky, carries a wealth of benefits that can set the foundation for a resilient and sustainable business. By relying on your own capabilities and resources, you make choices that align closely with your vision, ensuring that every decision reflects your core values.

One of the most significant advantages of bootstrapping is the control it affords. When you fund your business without outside investment, you retain complete authority over your operations and direction. This independence means you can pivot quickly in response to market changes or customer feedback without having to answer to investors or stakeholders. Your business can evolve organically, driven by your insights rather than external pressures.

Another compelling benefit is the development of financial discipline. Bootstrapping forces you to manage your cash flow meticulously and prioritize essential spending. This practice not only fosters a culture of frugality but also encourages innovative problem-solving. Entrepreneurs often discover creative ways to stretch their resources, leading to efficient processes and ultimately, a leaner operation. Over time, this financial savvy can prove invaluable as your business grows.

Moreover, bootstrapping cultivates a deep sense of commitment and ownership. When you invest your own money and resources into your business, your stakes are higher. This personal investment can bolster your motivation and drive, pushing you to work harder and persevere through challenges. The relationship you build with your venture becomes far more personal, often leading to greater satisfaction and fulfillment as you watch it flourish.

Bootstrapping Benefits

Description

Control

Full authority over business decisions and direction.

Higher personal investment leads to increased motivation.

Resilience

Builds a strong foundation for handling future challenges.

Furthermore, bootstrapping can enhance your business’s resilience. When your operation relies on your own resources, you learn to navigate challenges and setbacks independently. This experience fosters a problem-solving mindset, equipping you with the skills needed to adapt to market fluctuations. Businesses built on a strong foundation of resilience are often better positioned to weather economic downturns and unexpected disruptions.

Lastly, bootstrapping can forge a robust community and customer base. As you grow your business through your own resources, you tend to cultivate a loyal clientele that appreciates your authenticity and commitment. Customers often resonate with stories of self-made success, which can lead to strong brand loyalty and advocacy. This organic growth can be more sustainable than that driven by external funding, as it relies on genuine relationships rather than transactional interactions.

Identifying Your Unique Value Proposition to Stand Out

In a crowded marketplace, where countless entrepreneurs vie for attention, identifying and articulating your unique value proposition (UVP) is crucial for your business’s success. Your UVP serves as the guiding light, illuminating the specific benefits that set your offerings apart from the competition. It’s more than just a catchy tagline; it’s the compelling reason why potential customers should choose you over others.

To effectively define your UVP, start by asking yourself a few key questions:

What problem does my product or service solve?

Who is my target audience, and what are their pain points?

What unique features or benefits does my offering provide?

How do my values align with my customers’ expectations?

Once you have clarity on these points, distill them into a concise statement that highlights your distinctive qualities. This UVP should resonate with your audience’s needs and aspirations, effectively communicating the value they will receive. Remember, clarity trumps complexity—your message should be simple yet impactful.

Next, consider the emotional connection your business can create with its customers. People often make purchasing decisions based on feelings rather than logic. By incorporating elements that evoke emotion, such as storytelling or relatable experiences, you can strengthen your UVP. Think about the stories behind your brand—what inspired you to start this journey? Sharing these narratives can create a deeper bond with your audience.

It’s also vital to validate your UVP through market research. Engage with your target audience directly, gathering feedback on what they value most. This could be through surveys, focus groups, or social media polls. Understanding customer perspectives will not only refine your UVP but also foster a sense of community and loyalty among your customer base.

Lastly, ensure that your UVP is consistently communicated across all marketing channels. Whether it’s on your website, social media, or promotional materials, a cohesive message reinforces your brand identity and helps customers remember what makes you unique. Utilize visuals, testimonials, and case studies to enhance your UVP’s effectiveness and make your offerings more relatable.

a well-defined UVP not only helps you stand out but also serves as a foundation for all your business strategies. Take the time to articulate it clearly, validate it with your audience, and present it consistently. By doing so, you’ll not only attract more customers but also foster lasting relationships that can propel your business forward.

Creating a Lean Business Model to Maximize Resources

When embarking on a bootstrapping journey, the goal is to optimize every resource at your disposal. Creating a lean business model is essential, as it helps you streamline operations, minimize waste, and focus on what truly matters. Here’s how to effectively utilize your resources while building your business.

First, identifying your core offerings is crucial. Focus on the products or services that provide the most value to your customers. This not only helps in maximizing your existing resources but also allows you to establish a strong market presence. Consider the following steps:

Conduct market research to understand customer needs.

Analyze competitors to identify gaps in the market.

Test your offerings with a small audience to gather feedback.

Next, adopt a minimalist approach to operations. This means eliminating unnecessary expenses and focusing on essential activities that drive growth. Tools and techniques to consider include:

Implementing automation for routine tasks to save time.

Utilizing cloud-based services to reduce IT costs.

Outsourcing non-core activities to freelancers or specialized agencies.

Another key aspect of a lean business model is fostering a culture of innovation within your team. Encourage creative problem-solving and brainstorming sessions to uncover new ideas that can enhance efficiency. For example, consider forming cross-functional teams that allow employees from different departments to collaborate on projects. This cross-pollination of ideas can lead to innovative solutions and better use of resources.

Let’s not forget the importance of data-driven decision-making. Utilize analytics to track performance metrics and customer behavior. This information can guide your strategic choices, allowing you to allocate resources more effectively. Here’s a simple table illustrating some key performance indicators (KPIs) you might track:

Metric

Description

Customer Acquisition Cost (CAC)

Total cost of acquiring a new customer.

Lifetime Value (LTV)

Total revenue expected from a customer over their engagement.

Churn Rate

Percentage of customers who stop using your product/service.

don’t underestimate the power of community building. Engaging with your audience can create loyal customers who not only purchase from you but also serve as brand advocates. Use social media, newsletters, and local events to foster these connections. The feedback and insights you gain from your community are invaluable, often providing new ideas for product improvements and marketing strategies.

Funding Your Startup: Creative Ways to Bootstrap

Starting a business can feel like a daunting challenge, especially when funds are tight. However, bootstrapping offers a unique opportunity to launch and grow your startup using creativity and resourcefulness. Here are some innovative methods to fund your venture without relying on external investors.

1. Pre-Sell Your Product: Why wait until you have a fully developed product? Launch a pre-sale campaign to gauge interest and generate cash flow. Use social media and crowdfunding platforms to promote your idea. This not only helps in funding your project but also validates your market.

2. Tap into Your Network: Don’t overlook the power of your personal connections. Friends and family can be a great source of initial funding. Consider asking them for small loans or investments. Be transparent about your plans and how you intend to repay them. This helps maintain trust and accountability.

3. Offer Your Services: If you have a skill or service to offer, consider freelancing while you build your startup. This can provide you with a steady income stream and give you time to develop your product. Sites like Upwork and Fiverr can connect you with clients looking for your expertise.

4. Utilize Free Tools: There are countless free online resources that can help reduce your startup costs. From project management tools like Trello to graphic design software like Canva, leveraging free tools can save you money and help you focus your limited budget on growth activities.

5. Build a Community: Start networking early. Join local business groups, attend meetups, or engage with online forums. Building a community can lead to partnerships, mentorships, and even referrals that may open doors to new opportunities for funding and growth.

6. Bootstrap Your Marketing: Instead of spending on ads, focus on organic marketing strategies. Create valuable content, engage with your audience on social media, and leverage email marketing to nurture leads. This approach is often more sustainable and can yield better long-term results without breaking the bank.

Funding Method

Pros

Cons

Pre-Selling

Validates demand

Requires marketing effort

Network Funding

Trust factor is high

May strain relationships

Freelancing

Immediate cash flow

Time-consuming

Free Tools

Cost-effective

Limited features

Every penny counts when you’re bootstrapping. Embrace a frugal mindset and be mindful of your spending. Keep a close eye on your cash flow and prioritize expenses that drive growth. Your ability to stretch resources creatively can often be the difference between survival and success.

Building a Strong Network: Leveraging Connections for Success

Building a robust network can be a game-changer for entrepreneurs, especially those who are bootstrapping their way to success. The relationships you cultivate can provide invaluable resources, mentorship, and even funding opportunities. Here’s how to leverage your connections effectively:

Identify Key Players: Focus on individuals who are influential in your industry. This could be other entrepreneurs, potential clients, or thought leaders.

Engage Regularly: Consistent communication is essential. Attend events, engage on social media, and don’t hesitate to reach out with updates or to offer assistance.

Offer Value: Networking is a two-way street. Think about what you can bring to the table. This could be sharing insights, offering skills, or connecting people within your network.

Finding opportunities in unexpected places can also amplify your networking efforts. Consider non-traditional venues such as local meetups, online forums, and even your own community events. Each interaction is a potential stepping stone toward a valuable connection.

Additionally, consider leveraging platforms like LinkedIn to expand your reach. By joining industry-specific groups, you can share your knowledge, ask for advice, and tap into a broader audience. This digital networking can open doors that you may not have considered, especially when bootstrapping your business.

Networking Opportunity

Potential Benefit

Local Business Meetups

Direct connections with potential clients and partners

Online Webinars

Access to industry insights and expert advice

Professional Associations

Networking with established professionals in your field

Social Media Groups

Engagement with a broader audience for collaboration

As you build these relationships, remember that authenticity is key. People resonate with genuine connections over transactional interactions. Share your journey openly, and don’t shy away from discussing the challenges you face while bootstrapping your business. You might be surprised by how willing others are to lend a hand or share their experiences.

always be prepared to follow up. After meeting someone new, whether in person or online, send a brief note to express your appreciation for their time. This small gesture can solidify your connection and keep you top-of-mind when opportunities arise. A strong network is not just about quantity; it’s about the quality of the relationships you nurture.

Effective Marketing on a Budget: Strategies That Work

When you’re working with limited resources, effective marketing becomes not just a goal, but a necessity. Bootstrapping your business means you’re going to need to be resourceful, innovative, and strategic in your approach. Here are some proven strategies that can help you market effectively without breaking the bank:

Leverage Social Media: Choose platforms that align with your target audience and engage regularly. Create valuable content that resonates with your followers to foster community and loyalty.

Content Marketing: Start a blog or produce helpful guides that showcase your expertise. This not only establishes credibility but can also improve your SEO, drawing in organic traffic without the need for paid ads.

Email Marketing: Build an email list and send out regular newsletters with valuable content, promotions, and updates. This keeps your audience engaged and encourages repeat business.

Networking: Attend local events, trade shows, or virtual meetups. Building relationships can lead to partnerships, referrals, and insights that may not be accessible otherwise.

User-Generated Content: Encourage your customers to share their experiences with your products or services on social media. This not only promotes your brand but adds authenticity and trust.

To maximize your efforts, identify your unique selling proposition (USP) and communicate it effectively. This clarity will help you stand out in a crowded market and attract your ideal customers.

Additionally, consider implementing a referral program. Happy customers are often your best marketers. Incentivizing them to refer friends can lead to a cost-effective way to reach new audiences.

remember to track your marketing efforts. Utilize free tools like Google Analytics to assess what strategies are driving traffic and conversions. This data will guide your decisions and help you allocate resources more effectively.

Marketing Strategy

Cost

Expected Outcome

Social Media Engagement

Low

Increased brand awareness

Content Creation

Low to Medium

Improved SEO & authority

Email Campaigns

Low

Higher customer retention

Networking Events

Medium

New partnerships & leads

Referral Programs

Low

Increased customer base

By adopting these strategies, you can effectively market your business on a budget. Remember, the key is to be consistent, creative, and adaptable. The resources you have may be limited, but with the right approach, your potential for success is limitless.

Mastering Time Management: Prioritizing Tasks for Growth

When you’re venturing into the world of entrepreneurship with limited resources, mastering the art of time management becomes critical. Prioritizing tasks effectively can set the tone for your startup’s growth. It’s essential to identify which actions will yield the most significant results and focus your energy there. Here are some strategies to help you navigate your daily responsibilities:

Identify Your Goals: Clearly define what you want to achieve in the short and long term. This clarity will guide your decision-making process.

Use the Eisenhower Matrix: Categorize tasks into four quadrants—urgent and important, important but not urgent, urgent but not important, and neither. This will help you allocate your time wisely.

Set Deadlines: Establish realistic deadlines for each task. This will create a sense of urgency and help maintain momentum, preventing procrastination.

Limit Distractions: Identify common distractions in your workspace and take steps to minimize them. This can significantly boost your productivity.

Once you’ve prioritized your tasks, it’s time to take action. Start with ‘Quick Wins’: Focus on tasks that can be completed quickly and easily. These will build momentum and motivate you to tackle more complex projects. Additionally, consider breaking larger tasks into smaller, manageable chunks. This not only makes them less overwhelming but also allows for incremental progress.

Another vital aspect of time management is regular reflection. Schedule time weekly to evaluate your progress and adjust your plans accordingly. Ask yourself questions like:

What tasks took longer than expected?

Which activities contributed most to my goals?

What can I improve next week?

This reflection helps create a feedback loop that enhances your ability to prioritize effectively over time. You can also utilize tools and software designed for task management to streamline your processes. Popular options include Asana, Trello, and Notion, which can help you visualize your tasks and deadlines in a way that suits your workflow.

remember that time management is not just about work; it’s also essential to allocate time for rest and self-care. A well-rounded approach ensures that you stay energized and focused, which is crucial for sustainable growth. Consider implementing a time-blocking method where you schedule both work and rejuvenation activities into your calendar.

By mastering these time management strategies and prioritizing your tasks effectively, you create a foundation for growth that is sustainable and aligned with your goals. Embrace the journey, and watch your business flourish!

Using Technology to Streamline Operations and Cut Costs

In today’s fast-paced business landscape, leveraging technology isn’t just a luxury—it’s a necessity. By adopting various innovative tools and solutions, businesses can significantly enhance their operational efficiency while simultaneously slashing unnecessary costs. This approach is especially beneficial for startups and small companies that are navigating the challenging waters of bootstrapping.

One of the most effective ways to streamline operations is through the use of automation tools. By automating repetitive tasks, you can free up valuable time and resources that can be redirected towards growth initiatives. Consider implementing:

Customer Relationship Management (CRM) systems: These systems help manage customer interactions and data throughout the customer lifecycle, improving relationships and retention.

Email marketing automation: Automate your email campaigns to engage customers without the hassle of sending each message manually.

Accounting software: Simplifies financial tasks such as invoicing, expense tracking, and reporting, allowing you to focus on other core business activities.

Another crucial aspect is the adoption of cloud-based solutions. These platforms provide scalable resources that can grow alongside your business without the hefty investments associated with traditional IT infrastructure. Key benefits include:

Cost efficiency: Only pay for what you use, reducing overhead costs.

Accessibility: Access your data and applications from anywhere, facilitating remote work and collaboration.

Furthermore, adopting collaboration tools can significantly enhance team productivity. Tools like Slack, Trello, or Asana enable seamless communication and project management, ensuring everyone is on the same page. This can lead to quicker decision-making and reduced project turnaround times. Here’s a simple comparison of popular options:

Tool

Key Features

Best For

Slack

Real-time messaging, file sharing

Team communication

Trello

Visual project boards, task tracking

Project management

Asana

Task assignments, due dates, progress tracking

Team collaboration

Lastly, don’t overlook the potential of data analytics. By utilizing tools that provide insights into customer behavior and operational performance, you can make informed decisions that enhance efficiency and drive growth. Analyzing data can help you identify areas for improvement, optimize your resources, and ultimately reduce costs. Incorporate analytics into your strategy to stay ahead of the competition and refine your offerings based on real feedback.

By embracing these technologies, you not only streamline your operations but also position your business for sustainable growth. In the bootstrapping phase, every dollar and minute counts—ensuring that you are operating efficiently can lead to significant advantages in an ever-evolving market.

Learning from Failure: Embracing Risks in Your Bootstrapping Journey

In the world of entrepreneurship, failure is often a stepping stone rather than an endpoint. When you’re bootstrapping your business, the stakes can feel high, but with every misstep comes an invaluable lesson. Embracing risks means that you’re open to experimenting, innovating, and ultimately discovering what works best for you and your venture. The key lies in your response to those bumps in the road.

Many successful entrepreneurs will tell you that their greatest achievements were born from moments of failure. When you face setbacks, consider them as opportunities to:

Identify weaknesses: Analyze what went wrong and figure out how to strengthen those areas.

Adapt your strategy: Use insights from failures to pivot your approach and refine your business model.

Build resilience: Each challenge faced makes you more capable of handling future hurdles.

Encourage innovation: Sometimes, failure leads to unexpected creativity and solutions that you wouldn’t have considered otherwise.

Take, for example, the story of a bootstrapped startup that launched a product without fully understanding its target market. Initial sales were dismal, but instead of giving up, the founders sought feedback from customers. They learned crucial insights that allowed them to rebrand and reposition their product, leading to a successful relaunch. This scenario illustrates that embracing risk can provide the necessary data to make informed decisions moving forward.

Furthermore, developing a “fail fast, learn fast” mentality is essential. This approach encourages you to test ideas quickly and learn from the outcomes without investing excessive time or resources. By iterating based on feedback and real-world results, you can make smarter choices about where to focus your efforts. Consider setting up small-scale experiments or pilot programs that allow you to gauge responses before committing fully. This strategy not only mitigates risk but fosters a culture of continuous improvement.

Action

Benefit

Analyze Each Failure

Gain insights for future decisions

Encourage Feedback

Improve product-market fit

Iterate Quickly

Enhance efficiency and effectiveness

Celebrate Small Wins

Build morale and confidence

As you navigate your bootstrapping journey, remember that every entrepreneur experiences setbacks. What sets successful entrepreneurs apart is their ability to stay positive and remain focused on their long-term vision. By viewing failures as learning experiences, you can cultivate a growth mindset. This mindset not only empowers you but also inspires your team and builds a resilient organizational culture that thrives on challenges.

Ultimately, to truly embrace risks in your bootstrapping journey, you must be willing to step out of your comfort zone. Challenge yourself to take calculated risks that may lead to transformative ideas and solutions. The road may not always be smooth, but with each stumble, you’re one step closer to success.

Scaling Your Business: When and How to Seek Outside Funding

As your business begins to grow, you might find yourself at a crossroads regarding funding. While bootstrapping has its advantages, there comes a time when relying solely on personal funds may not suffice for scaling. Understanding when and how to seek outside funding is crucial. Here are some insights on this important decision.

First, it’s essential to identify key growth indicators. These could include:

Increased demand: Are you consistently turning away customers?

Saturation of the market: Do you see competitors gaining the edge?

Expansion opportunities: Are there new markets or products you can pursue?

Once you identify these indicators, assess your current financial health. A comprehensive evaluation can help you understand whether outside funding is the right move. Look for:

Revenue trends: Are your profits steadily increasing?

Cash flow management: Are you able to cover operational costs without strain?

Future projections: Is there a sustainable growth plan in place?

When you’re ready to explore external funding, consider your options. Different sources come with their advantages and drawbacks:

Funding Source

Pros

Cons

Angel Investors

Mentorship, networks

Equity dilution

Venture Capital

Large amounts of capital

Pressure for rapid growth

Bank Loans

Retain equity

Repayment obligations

Crowdfunding

Market validation

Time-consuming

Once you choose a funding source, refine your pitch. Potential investors are often interested in:

Your business model: Clearly outline how you make money.

Your value proposition: What sets you apart from the competition?

Your growth strategy: How do you plan to use the funds to scale?

remember that seeking outside funding isn’t just about the money—it’s about building relationships. The right investors can provide invaluable guidance and resources. Approach this process with openness and be ready to share your vision and your passion.

Real-Life Success Stories: Inspiration from Bootstrapped Businesses

Bootstrapped businesses often navigate a unique path, driven by resourcefulness and unwavering determination. One of the most inspiring examples is Basecamp, originally founded as 37signals. The company started with a simple idea: to create a project management tool that emphasized simplicity and clarity. By leveraging their own resources and focusing on customer feedback, they transformed Basecamp into a must-have tool for teams worldwide, all without external funding.

Another remarkable case is that of Mailchimp. Launched in 2001 as a side project while the founders ran a web design firm, Mailchimp grew organically by focusing on customer needs. They provided a user-friendly email marketing platform that catered to small businesses, emphasizing ease of use and affordability. Today, Mailchimp serves millions of users globally, proving that a strong product paired with smart marketing can yield tremendous success without outside investment.

Spanx, the celebrated shapewear brand, is a quintessential example of bootstrapping success. Founded by Sara Blakely with just $5,000, Spanx started with a simple pair of footless pantyhose. Blakely’s ingenuity in marketing, her relentless pursuit of quality, and her ability to bootstrap her way to the top led to a billion-dollar valuation, making her one of the youngest self-made female billionaires in the world.

These stories highlight a few essential strategies that bootstrapped businesses often employ to thrive:

Focus on Customer Needs: Understanding what customers want is crucial. Businesses that listen and adapt their offerings flourish.

Lean Operations: Operating on a tight budget forces companies to minimize waste, streamline processes, and innovate.

Iterative Development: Rather than launching a perfect product, bootstrapped companies often iterate based on feedback, allowing for continuous improvement.

Additionally, the journey of Patagonia illustrates the power of purpose in a bootstrapped business. Founded by Yvon Chouinard, Patagonia began as a small company selling climbing gear. Its commitment to environmental sustainability and ethical production practices attracted a loyal customer base. By reinvesting in their mission rather than seeking external funding, Patagonia grew into a major player in the outdoor apparel market while remaining true to its values.

The triumphs of these companies showcase that with creativity, grit, and a strong vision, bootstrapped businesses can not only survive but thrive in competitive landscapes. Each success story serves as a reminder that the best resources may not always come from traditional funding avenues but from the passion and ingenuity of the founders themselves.

Practical Tips for Maintaining Motivation and Focus

Staying motivated and focused while bootstrapping your business can be challenging, especially when resources are tight. Here are some practical strategies to help you maintain your drive:

Set Clear Goals: Break your larger vision into smaller, manageable milestones. This will help you track progress and maintain focus on immediate tasks.

Create a Routine: Establish a daily routine that prioritizes your most important tasks. Consistency can enhance productivity and help you stay on track.

Limit Distractions: Identify what disrupts your focus, whether it’s social media, noise, or other interruptions. Use tools like website blockers or create a dedicated workspace to minimize these distractions.

Stay Connected: Engage with fellow entrepreneurs or like-minded individuals. Sharing experiences and challenges can provide fresh perspectives and support, keeping your motivation levels high.

Celebrate Small Wins: Acknowledge and reward yourself for achieving small milestones. This can reinforce positive behavior and keep your morale soaring.

Another effective way to maintain focus is to practice mindfulness. Taking a few moments each day to reflect or meditate can clear your mind, helping you prioritize what truly matters. Consider techniques like:

Deep Breathing: A few minutes of deep breathing can help calm your mind and sharpen your focus.

Short Breaks: Implement the Pomodoro Technique: work for 25 minutes and take a 5-minute break.

Gratitude Journaling: Writing down things you’re grateful for can shift your mindset to a more positive one, boosting motivation.

Lastly, it’s essential to remember that maintaining motivation is a dynamic process. As circumstances change and challenges arise, being adaptable is vital. Here’s a simple table to illustrate how you can adjust your focus as needed:

Challenge

Adaptive Strategy

Feeling Overwhelmed

Break tasks into smaller steps and prioritize

Loss of Interest

Reconnect with your initial motivation and vision

Distractions

Create a focused workspace and set boundaries

Lack of Progress

Reassess goals and adjust timelines if necessary

By implementing these strategies, you’ll not only enhance your focus but also keep your enthusiasm alive as you bootstrap your business. Remember, it’s about progress, not perfection.

The Long-Term Vision: Planning for Sustainable Growth

Building a business from the ground up without external funding can be a daunting task, yet it offers unique advantages that can pave the way for sustainable growth. By focusing on self-sufficiency, entrepreneurs can foster a culture of innovation and resilience that becomes ingrained in the company’s DNA. To ensure long-term success, it’s essential to embrace a holistic approach to planning and resource management.

One key aspect of this long-term vision is establishing a clear roadmap that outlines your goals and milestones. Consider breaking down your objectives into manageable phases:

Short-term goals: Focus on immediate profitability and market presence.

Mid-term aspirations: Aim to expand your product line or enhance your service offerings.

Long-term objectives: Develop strategies for sustainable growth and adaptability in a changing market landscape.

Another crucial element is maintaining a lean operational model. By minimizing unnecessary expenses and optimizing processes, you can reinvest your profits into the business. This could involve:

Streamlining workflows to improve efficiency.

Utilizing technology to automate repetitive tasks.

Regularly reviewing and adjusting your budget to prioritize essential expenditures.

Moreover, building a strong customer relationship is vital for long-term sustainability. Engaging with your customers and understanding their needs can lead to brand loyalty and repeat business. Consider strategies such as:

Implementing a feedback loop to gather insights and improve offerings.

Creating community-focused events to build connections and trust.

Personalizing communications and promotions based on customer behavior.

Investing in your team is equally important. A motivated and skilled workforce is the backbone of any successful business. You can support their growth by:

Providing ongoing training and development opportunities.

Encouraging a collaborative and inclusive workplace culture.

Recognizing and rewarding achievements to boost morale.

Lastly, consider establishing a feedback mechanism for your business model. This involves regularly assessing your progress against your goals and being open to pivot or adapt strategies as necessary. Building a resilient business takes time, but with a commitment to monitoring your performance and making informed decisions, you can ensure that your venture not only survives but thrives for years to come.

Focus Area

Strategies

Operational Efficiency

Streamlining workflows, automating tasks

Customer Engagement

Feedback loops, community events

Team Development

Training programs, inclusive culture

Frequently Asked Questions (FAQ)

Q&A: What Is Bootstrapping in Business? How to Launch and Grow Using Only Your Own Resources

Q: What exactly is bootstrapping in business?

A: Great question! Bootstrapping is essentially a way of starting and growing a business using only your own resources without relying on external funding. Think of it as building your dream home with your own two hands—you’re using what you have at your disposal to create something incredible! This means you’re often funding your business through personal savings, revenue generated from early sales, or reinvesting profits back into the business.

Q: Why should entrepreneurs consider bootstrapping?

A: There are several compelling reasons! First, bootstrapping gives you complete control over your business. You’re not beholden to investors or banks, which means you can make decisions that align with your vision without outside pressure. Plus, it encourages creativity and resourcefulness. When you’re working with limited resources, you have to think outside the box and innovate to solve problems. It also helps you build a more sustainable business model. You’ll be focused on generating revenue from day one, which can lead to more stability down the road.

Q: What are some of the biggest challenges of bootstrapping?

A: While bootstrapping can be rewarding, it’s not without its challenges. One of the main hurdles is the financial strain. You may have to live frugally and put your personal finances on the line, which can be stressful. Additionally, growing a business without external funding may limit how quickly you can scale. This means you’ll need to be patient and strategic about your growth. It can also require a lot of hard work and long hours, especially if you’re managing multiple roles within your business.

Q: How can someone successfully bootstrap their business?

A: Success in bootstrapping starts with a solid plan. Focus on identifying a niche or problem you’re passionate about and create a minimum viable product (MVP) to test the waters. Make sure to keep your costs low—consider working from home or leveraging free tools and resources. Networking is also crucial; tap into your community for support and advice. Lastly, prioritize customer feedback and adapt your offerings to meet their needs. This will help ensure you’re putting your resources into what truly matters.

Q: Can you provide some examples of successful bootstrapped companies?

A: Absolutely! Some of the most iconic companies started out bootstrapped. For example, Mailchimp began as a side project and was self-funded by its founders. They focused on building a user-friendly email marketing platform and grew it into a multimillion-dollar business without taking any outside investment. Another great example is Basecamp, which started as a web design firm and evolved into a successful project management tool, all while being self-sustained.

Q: Is bootstrapping right for everyone?

A: Not necessarily! While bootstrapping can be a great strategy for many, it might not suit everyone or every business model. If you have a high-growth tech startup that requires significant upfront investment to develop your product, seeking outside funding might be the better route. However, if you’re passionate about your idea and willing to put in the time and effort to grow steadily, bootstrapping can be incredibly fulfilling. Ultimately, it boils down to your business goals, risk tolerance, and personal circumstances.

Q: Any final tips for aspiring bootstrappers?

A: Definitely! Stay focused on your core mission, be adaptable, and leverage your existing network for support. Remember to keep learning—be it through books, podcasts, or networking with other entrepreneurs. Lastly, celebrate your small wins along the way; they can fuel your motivation as you navigate the ups and downs of bootstrapping. With determination and smart strategies, you can build a thriving business using just your own resources!

To Conclude

bootstrapping can be a game-changer for aspiring entrepreneurs looking to turn their dreams into reality without relying on external funding. By leveraging your own resources, creativity, and determination, you can build a business that not only reflects your vision but also fosters independence and resilience. Remember, many successful companies started with just a handful of resources and a strong belief in their ideas.

As you embark on this journey, keep in mind that bootstrapping is not just about saving money—it’s about making smart, strategic decisions that align with your goals. Embrace the challenges, learn from your experiences, and celebrate every milestone, no matter how small.

So, are you ready to take the plunge? With your passion and a clear roadmap, you can launch and grow your business using the power of bootstrapping. Go ahead, take that first step, and watch your entrepreneurial dreams come to life!