Welcome to the world of small business bookkeeping—where numbers tell your story and financial clarity paves the way for success! If you’re a small business owner, you know that juggling daily operations, customer relationships, and marketing can feel like a full-time job in itself. But let’s face it: without a solid grip on your finances, all that hard work can quickly go to waste. That’s where effective bookkeeping steps in, transforming chaos into order and confusion into clarity.

In this essential guide, we’ll walk you through the key components of bookkeeping that every small business owner should know. Whether you’re just starting out or looking to refine your existing practices, understanding the fundamentals of bookkeeping can help you make informed decisions, boost profitability, and ultimately, achieve your business dreams. Ready to take control of your financial future? Let’s dive in!

Understanding the Importance of Accurate Bookkeeping for Small Businesses

Accurate bookkeeping is the backbone of any small business, serving as the foundation upon which financial health and strategic decision-making are built. Without it, navigating the complexities of business finances can feel like sailing in uncharted waters. Here’s why precision in bookkeeping is not just important, but essential for the survival and growth of small enterprises.

First and foremost, accurate bookkeeping ensures compliance with tax regulations. Small businesses are subject to various tax laws, and maintaining precise records helps in filing taxes accurately and on time. This minimizes the risk of penalties and audits, allowing business owners to focus on growth rather than worrying about legal troubles.

Moreover, effective bookkeeping provides a clear view of cash flow. Understanding your cash flow is crucial for making informed decisions. Regularly updated records allow entrepreneurs to track income and expenses, helping to identify trends over time. This transparency enables businesses to forecast future cash needs and avoid potential shortfalls.

Another vital aspect is that proper bookkeeping enhances budgeting and financial planning. By analyzing past financial data, small business owners can create realistic budgets and set achievable financial goals. Here are some budgeting benefits that stem from accurate bookkeeping:

Identifying unnecessary expenses

Allocating resources more effectively

Pinpointing areas for investment and growth

Additionally, sound bookkeeping practices can significantly improve your access to financing. When applying for loans or attracting investors, having organized financial statements demonstrates professionalism and reliability. Lenders and investors often require detailed financial reports, and accurate bookkeeping makes this process seamless.

Benefit

Impact on Business

Tax Compliance

Reduces the risk of audits and penalties

Cash Flow Management

Helps avoid financial shortfalls

Budget Planning

Facilitates resource allocation and growth

Financing Opportunities

Increases chances for loans and investment

Lastly, accurate financial records can assist in improving overall business efficiency. When bookkeeping is done correctly, it reduces the time spent on financial management and allows business owners to dedicate more resources to strategic planning and operations. This leads to better service delivery and increased customer satisfaction.

the significance of meticulous bookkeeping cannot be overstated. It empowers small business owners to not only survive but thrive in a competitive landscape. By investing in accurate record-keeping practices, entrepreneurs can lay a solid groundwork for sustainable success.

Essential Bookkeeping Terms Every Small Business Owner Should Know

Running a small business involves juggling numerous tasks, and understanding the basic terminology of bookkeeping can significantly ease that burden. Here are some essential terms every small business owner should familiarize themselves with to ensure their financial management is on point.

Accounts Receivable refers to the money that your customers owe you for products or services delivered but not yet paid for. Keeping track of accounts receivable is crucial, as it directly affects your cash flow and overall profitability. A well-organized system can help you avoid late payments and maintain strong customer relationships.

Accounts Payable is the flip side of accounts receivable. This term encompasses the money your business owes to suppliers and creditors for goods or services received. Managing accounts payable efficiently can improve your vendor relationships and ensure that your business maintains a good credit rating.

Balance Sheet is a snapshot of your business’s financial health at a specific point in time. It lists your assets, liabilities, and equity, providing a clear picture of what you own versus what you owe. This document is invaluable for potential investors and can help you make informed decisions about your business’s future.

Income Statement, also known as a profit and loss statement, summarizes your revenues and expenses over a specific period. This document helps you determine your profitability and can guide strategic decisions, such as cutting costs or investing in growth opportunities.

Cash Flow refers to the movement of money in and out of your business. Positive cash flow indicates that your business has enough liquidity to meet its obligations, while negative cash flow can signal financial trouble. Monitoring cash flow is essential for maintaining operational stability and making informed financial decisions.

To better understand these concepts, here’s a simple comparison of key financial statements:

Statement

Purpose

Frequency

Balance Sheet

Shows financial position

Monthly/Quarterly/Annually

Income Statement

Tracks profitability

Monthly/Quarterly/Annually

Cash Flow Statement

Monitors cash movement

Monthly/Quarterly

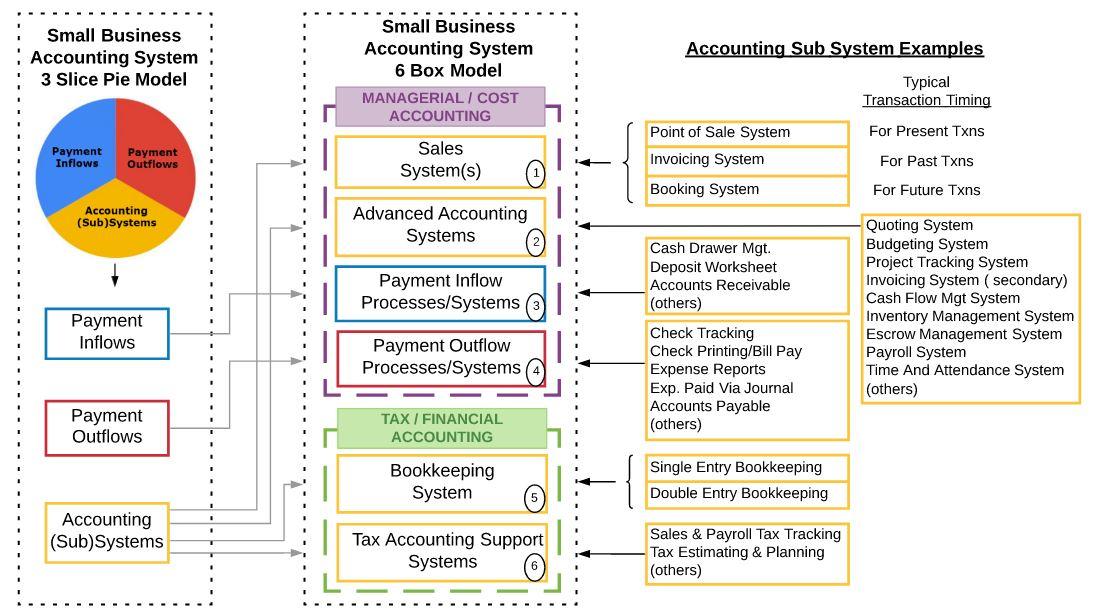

General Ledger serves as the central repository for all your financial transactions. It includes accounts for assets, liabilities, equity, revenues, and expenses, providing a comprehensive overview of your business’s financial activities. Regularly updating your general ledger is crucial for accurate financial reporting.

Lastly, don’t overlook the importance of Reconciliation. This process involves comparing your financial records against bank statements and other external documents to ensure accuracy. Regular reconciliation helps identify discrepancies early, preventing potential financial mismanagement.

Choosing the Right Accounting Method: Cash vs. Accrual

When it comes to managing your small business’s finances, one of the most critical decisions you’ll make is choosing between cash and accrual accounting methods. Each method has its pros and cons, and understanding these can significantly impact your financial reporting and tax obligations.

Cash Accounting is the simplest of the two methods. With cash accounting, you record income and expenses only when money actually changes hands. This means you’ll recognize revenue when you receive payments and expenses when you pay bills. Here are some benefits of cash accounting:

Simplicity: It’s easy to maintain and understand, making it ideal for small business owners without an accounting background.

Immediate Cash Flow Insight: You get a clear picture of your cash flow, as you are only tracking money that is physically in your hands.

Tax Benefits: You only pay taxes on income that you’ve actually received, which can be beneficial for cash-strapped businesses.

However, cash accounting does have its limitations. It doesn’t provide a complete picture of your financial health, as it can overlook outstanding invoices and future obligations. This could lead to potential cash flow issues if you’re unaware of income that’s owed to you. Now, let’s look at the other side of the coin.

Accrual Accounting, on the other hand, recognizes revenue and expenses when they are incurred, regardless of when the cash is received or paid. This method is generally more complex but offers a more accurate representation of your business’s financial status. Here’s why you might consider accrual accounting:

Comprehensive Financial Picture: It provides a fuller view of your business’s profitability and financial position.

Better Decision-Making: You can make more informed decisions based on the revenue and expenses that are expected, not just what is currently in the bank.

Compliance: Many larger businesses and corporations are required to use accrual accounting, so adopting this method early can prepare you for future growth.

However, accrual accounting isn’t without its challenges. Tracking accounts payable and receivable can become cumbersome, and you might find it harder to predict your cash flow. In addition, you may face tax liabilities on income you haven’t yet received, which could strain your financial resources.

To make an informed choice, consider your business model, size, and financial needs. If your operations are straightforward and you have minimal inventory, cash accounting might be suitable. On the flip side, if you have extensive transactions, long-term contracts, or need to manage inventory, accrual accounting may be the better option.

Ultimately, the right accounting method for your small business will depend on your unique situation. Evaluating the pros and cons of each will help you make a decision that aligns with your business goals and financial strategies.

Setting Up Your Bookkeeping System: DIY or Hire a Professional?

When it comes to managing your small business finances, one of the first decisions you’ll face is whether to tackle bookkeeping yourself or hire a professional. Both options have their pros and cons, and the best choice depends on your unique situation. Let’s explore the key factors to help you decide.

First, consider the complexity of your business transactions. If you’re running a simple operation with straightforward income and expenses, you might find that a DIY approach is manageable. However, as your business grows or if you deal with multiple revenue streams, sales tax, or payroll, the need for expertise becomes more pressing.

Time Commitment: DIY bookkeeping can be time-consuming. Are you prepared to dedicate hours each week to keeping your books up to date?

Understanding of Financial Regulations: Keeping up with tax laws and regulations can be daunting. A professional will have the knowledge to help you avoid costly mistakes.

Software Savvy: Are you comfortable using accounting software? If not, a professional can not only use it but also recommend the best tools for your needs.

On the flip side, hiring a professional can offer significant advantages. You gain access to their expertise and save time, allowing you to focus on what you do best—growing your business. Here are some benefits of bringing in a pro:

Accuracy: Professionals are trained to spot errors and discrepancies, ensuring your financial records are accurate and reliable.

Tax Planning: They can help you plan for taxes throughout the year, potentially saving you money and avoiding surprises during tax season.

Customized Reporting: A professional can provide tailored financial reports, giving you insights into your business’s performance.

To help you weigh your options, here’s a quick comparison of the two approaches:

Criteria

DIY

Hire a Professional

Cost

Lower expenses initially

Higher costs but may save money in the long run

Time

Time-consuming

Time-efficient

Expertise

Limited to your knowledge

Extensive knowledge and experience

Flexibility

Complete control

May have to work around availability

Ultimately, the choice between DIY bookkeeping and hiring a professional boils down to your specific business needs, your financial knowledge, and how much time you’re willing to invest. If you decide to go the DIY route, ensure you educate yourself about basic accounting principles and invest in reliable software. On the other hand, if you choose to hire someone, take the time to find a qualified professional who understands your industry and can add value to your operations.

The Role of Bookkeeping Software: Finding the Best Fit for Your Business

Choosing the right bookkeeping software can make or break your small business. With the growing number of options available, it’s crucial to find a solution that aligns not only with your financial needs but also with your operational style. The ideal software should simplify your accounting processes, enabling you to focus on growth and customer satisfaction.

When exploring different bookkeeping solutions, consider the following features:

User-Friendly Interface: A straightforward and intuitive design saves you time and frustration.

Integration Capabilities: Ensure it connects seamlessly with other tools you use, such as your payment processors and eCommerce platforms.

Automation: Features like automated invoicing and expense tracking can drastically reduce manual work.

Reporting Tools: Robust reporting can give you insights into your business’s financial health at a glance.

Customer Support: Reliable support can help you troubleshoot any issues quickly, keeping your operations running smoothly.

One of the most significant advantages of modern bookkeeping software is its ability to provide real-time financial information. This feature allows you to make informed decisions based on up-to-date data. Imagine having access to your cash flow status or profit margins at any moment. This level of transparency can empower you to strategize more effectively and respond to market changes promptly.

Moreover, let’s not forget about compliance. Many software solutions offer built-in compliance features that help you stay aligned with tax laws and regulations. This can significantly reduce the risk of errors that could lead to costly penalties. A system that updates automatically with the latest regulations can save you from the headache of manual updates.

To illustrate the importance of choosing the right software, here’s a quick comparison table of popular options:

Software

Best For

Starting Price

Key Features

QuickBooks

Small to Medium Businesses

$25/month

Invoicing, Expense Tracking, Reports

Xero

Startups

$12/month

Project Management, Inventory Tracking

FreshBooks

Freelancers

$15/month

Time Tracking, Client Portals

Wave

Small Businesses on a Budget

Free

Invoice Creation, Receipt Scanning

Each software has its unique strengths, catering to different types of businesses. Take the time to assess what capabilities you prioritize. This will ensure that you’re not only investing in a tool but in a partner that supports your vision for the business.

remember that adopting new software is a journey. Many platforms offer free trials, so take advantage of these opportunities to explore what fits best. Engaging your team during this process can also provide insights that highlight collective needs and preferences, ensuring a smoother transition and greater long-term satisfaction.

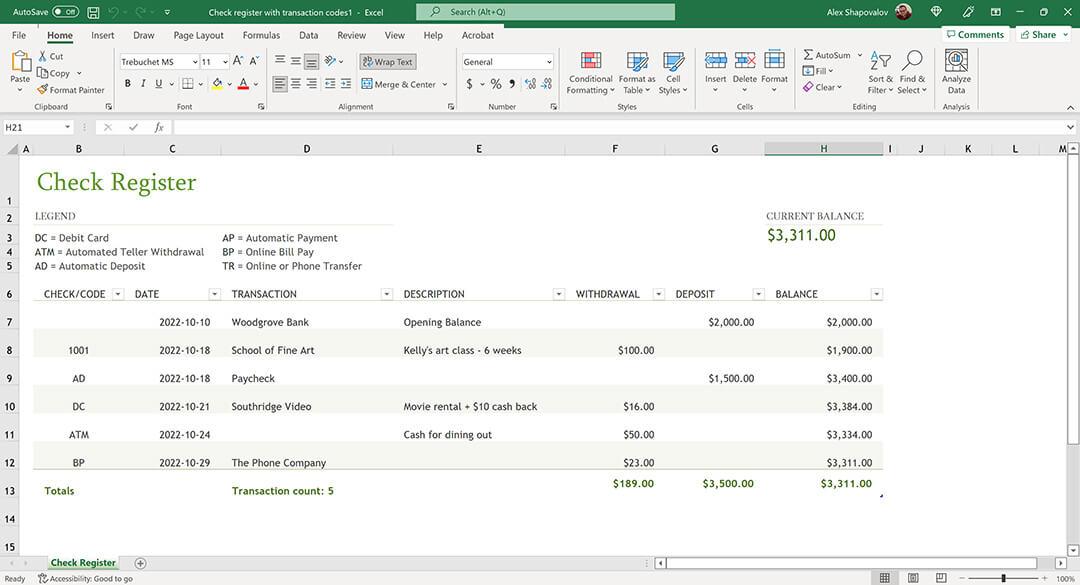

Mastering the Basics: Tracking Income and Expenses Effectively

Keeping a close eye on your financials is not just a necessity; it’s a vital part of running a successful small business. Tracking income and expenses effectively can provide you with insights that drive decision-making and strategy. Start by establishing a systematic approach that you can stick to. Here are some essential steps to get you on the right path:

Choose the Right Tools: Utilize accounting software like QuickBooks or FreshBooks, which can simplify the process of tracking your transactions. Alternatively, a well-organized spreadsheet can also suffice if you’re just starting out.

Separate Business and Personal Finances: Open a dedicated business bank account to keep your financial activities distinct. This will make it easier to manage your income and expenses without mixing personal transactions.

Document All Transactions: Whether it’s a sale, a supplier invoice, or a business expense, make it a habit to document every transaction. Look into using receipt scanning apps to keep your paper trail organized.

Regularly updating your records is equally crucial. Set aside time each week to enter your transactions. This not only keeps your records up to date but also helps you to stay aware of your financial situation. It’s easy to become overwhelmed if you let everything pile up until tax season!

Creating a simple table can help you keep track of your income and expenses effectively. For example:

Date

Description

Income

Expenses

01/02/2023

Product Sale

$500

01/05/2023

Office Supplies

$150

01/10/2023

Service Fee

$300

01/15/2023

Marketing

$200

Once you have a clear view of your income and expenses, analyzing trends becomes easier. Look for patterns in your financial data to identify peak income periods or unexpected expenses. This information can guide your budget planning and help you make informed business decisions.

Lastly, consider consulting a professional accountant periodically. They can offer valuable insights and help you set up a system that works best for your business needs. An expert can also assist with compliance issues and make sure your records are audit-ready.

Organizing Your Financial Records: Tips for Easy Access and Management

Managing your financial records doesn’t have to be a daunting task. With a few simple strategies, you can streamline the process and make it easier to access the information you need. Here are some practical tips to help you stay organized and on top of your small business bookkeeping.

Embrace Digital Solutions: In today’s technology-driven world, going digital can save you time and eliminate clutter. Consider using accounting software that allows you to:

Track expenses and income in real-time.

Store invoices and receipts electronically.

Generate reports with just a few clicks.

By transitioning to a digital format, you can access your records from anywhere, making it easier to manage your finances on the go.

Create a Structured Filing System: Whether you prefer paper or digital records, a well-structured filing system is crucial. Organize your files using categories that make sense for your business, such as:

Sales invoices

Expense receipts

Bank statements

Tax documents

This way, when you need to find a specific document, you won’t waste time searching through a disorganized pile.

Set a Regular Schedule: Consistency is key when it comes to managing your financial records. Set aside dedicated time each week or month to review your finances. This could include:

Reconciling your bank statements.

Updating your bookkeeping software.

Reviewing your cash flow and budgeting.

Regular check-ins will help you stay on top of your finances and catch any discrepancies early on.

Utilize a Simple Table for Tracking: Keeping track of your financial activities can be made easier with a simple tracking table. Here’s an example of a basic format:

Date

Description

Amount

Category

2023-10-01

Office Supplies

$150.00

Expenses

2023-10-05

Client Payment

$1,200.00

Income

This simple table can be part of your monthly review process, allowing you to easily see where your money is going and coming from.

Don’t Forget Backup: Whether you’re maintaining digital or physical records, always have a backup plan. Regularly back up your digital files to a secure cloud service or external drive. For paper records, consider scanning important documents and storing them digitally, so you always have a backup in case of loss or damage.

don’t hesitate to seek professional help if needed. A professional accountant can provide insights that save you time and money, ensuring your financial records are in tip-top shape.

Preparing for Tax Season: Bookkeeping Practices That Save You Money

Tax season doesn’t have to be a stressful time for small business owners. With the right bookkeeping practices in place, you can not only streamline the process but also save money in the long run. Here are some essential strategies to help you prepare effectively.

Organize Your Records: Keeping your financial documents organized is crucial. Consider creating a dedicated folder for:

Invoices and receipts

Bank statements

Payroll records

Expense reports

Use cloud storage solutions to easily access and back up your documents. This will save you time when it comes to gathering information for tax filing.

Track Your Expenses: Knowing where your money goes is vital for identifying potential deductions. Use accounting software or spreadsheets to categorize your expenses. This will help you pinpoint:

Deductible business expenses

Trends in spending

Areas to cut costs

Separate Business and Personal Finances: Mixing personal and business transactions can lead to a chaotic bookkeeping situation. Open a dedicated business bank account and credit card to make tracking easier. Keeping these finances separate helps in:

Avoiding tax-related complications

Providing clearer financial records

Improving your business’s credibility

Regular Reconciliation: Make it a habit to reconcile your accounts monthly. This practice involves matching your records with bank statements. It helps in identifying discrepancies early on and ensures your financial data is accurate. Consistency is key!

Consider Hiring a Professional: If bookkeeping feels overwhelming, don’t hesitate to seek help. A professional accountant can provide insights that might save you significant amounts during tax season. They can assist with:

Identifying tax deductions

Ensuring compliance with tax regulations

Providing strategic financial advice

Utilize Technology: Leverage accounting software tailored for small businesses. Many platforms offer features like automated invoicing, expense tracking, and tax preparation. Here’s a comparison table of popular options:

Software

Key Features

Price Range

QuickBooks

Invoicing, Reporting, Tax deductions

$25 – $150/month

Xero

Bank reconciliation, Expense claims

$12 – $65/month

FreshBooks

Time tracking, Client management

$15 – $50/month

By implementing these practices, you’ll not only be prepared for tax season but can also uncover opportunities to save money throughout the year. Stay proactive and make bookkeeping a priority to enjoy the benefits come tax time.

How to Create and Maintain a Budget for Your Small Business

Creating and maintaining a budget for your small business is not just about tracking expenses; it’s an essential strategy for ensuring your business’s longevity and growth. By establishing a clear budget, you can make informed decisions, identify potential financial pitfalls, and ultimately set your business up for success.

Start by determining your fixed and variable expenses. Fixed expenses are those that remain constant each month, such as rent and salaries, while variable expenses can fluctuate, like utility bills and inventory costs. Understanding these categories helps you accurately forecast your cash flow.

Once you have a handle on your expenses, it’s crucial to estimate your monthly income. This means not only considering current revenue but also projecting future earnings based on market trends and sales forecasts. A good practice is to create a table to visualize these amounts:

Category

Monthly Amount

Fixed Expenses

$3,000

Variable Expenses

$1,500

Projected Income

$5,000

With your expenses and income mapped out, it’s time to set some financial goals. Outline what you want to achieve through your budget—whether it’s increasing profits, saving for expansion, or reducing debt. Setting specific, measurable goals will keep you motivated and focused.

Now, automate your budgeting process. Utilize accounting software that allows you to track expenses in real-time, categorize transactions, and generate reports. This not only saves time but also minimizes errors, giving you a clearer picture of your financial health. Popular tools like QuickBooks and FreshBooks are great options for small business owners.

Don’t forget to review and adjust your budget regularly. As your business evolves, so will your financial needs. Set a recurring appointment on your calendar—monthly or quarterly—to assess your budget and make necessary changes. Being flexible will help you respond to market fluctuations and seize new opportunities.

consider involving your team in the budgeting process. Encourage input from employees who handle day-to-day operations. They might provide insights into potential cost savings or revenue opportunities you hadn’t considered.

Understanding Financial Statements: A Guide for Small Business Owners

When it comes to managing your small business, understanding financial statements is crucial. These documents not only provide a snapshot of your company’s financial health but also serve as valuable tools for decision-making. Let’s break down the key components you’ll encounter.

Balance Sheet

The balance sheet offers a glimpse into your business’s assets, liabilities, and equity at a specific point in time. This is where you’ll see what your company owns versus what it owes. Key elements include:

Assets: Everything of value your business owns, such as cash, inventory, and property.

Liabilities: Obligations or debts your business owes to others, like loans and accounts payable.

Equity: The residual interest in the assets of the business after deducting liabilities, essentially what the owners have invested.

Income Statement

The income statement, or profit and loss statement, provides insights on your business’s performance over a specific period. It highlights:

Revenue: The total income generated from sales or services.

Expenses: All costs incurred in the process of earning revenue, including salaries, rent, and utilities.

Net Income: The profit or loss after subtracting expenses from revenue, a clear indicator of your business’s profitability.

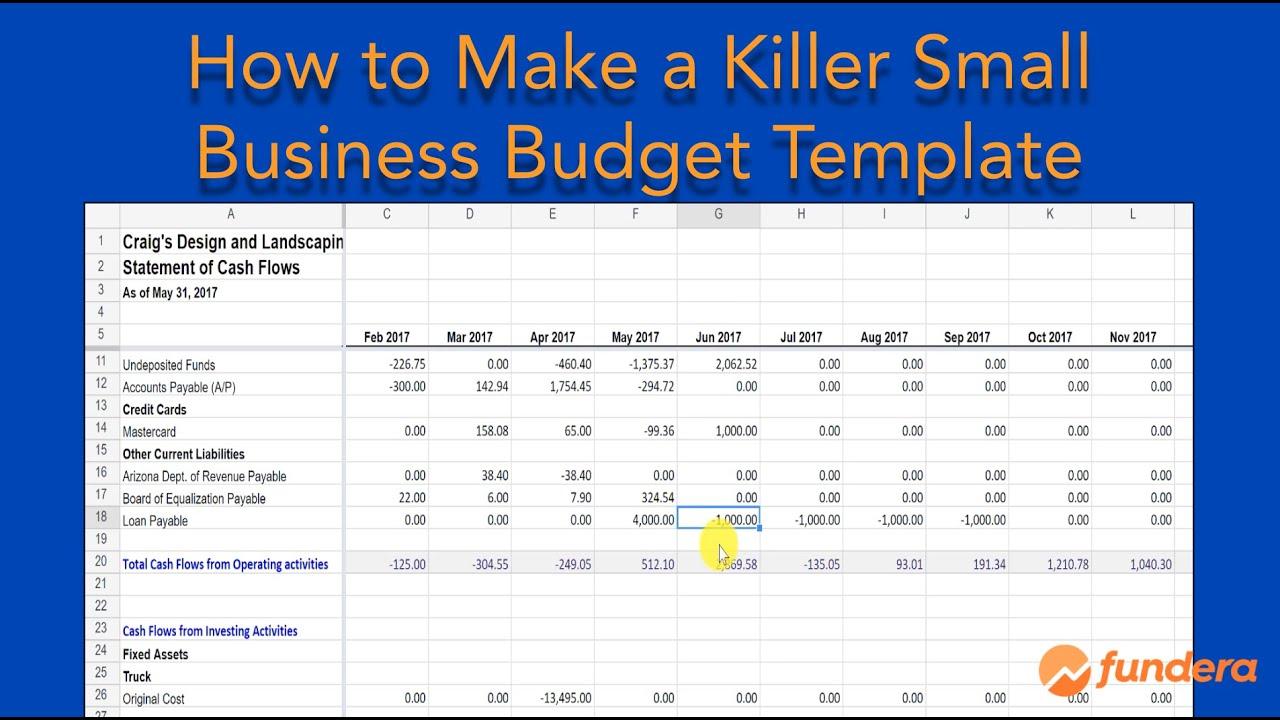

Cash Flow Statement

The cash flow statement tracks the flow of cash in and out of your business. It’s essential for understanding liquidity. Here are its three main components:

Operating Activities: Cash generated from your core business operations.

Investing Activities: Cash used in or generated from investments in assets, like purchasing equipment.

Financing Activities: Cash flows from borrowing or repaying debts or from issuing equity.

Utilizing Financial Statements

Understanding these statements allows you to make informed decisions. Regular analysis of your financial statements can help you:

Identify trends and patterns in your business.

Set realistic budgets and forecasts.

Evaluate your business’s performance against industry benchmarks.

Table: Key Financial Ratios

Ratio

Formula

What It Indicates

Current Ratio

Current Assets / Current Liabilities

Liquidity position of the business

Net Profit Margin

Net Income / Revenue

Profitability of the business

Return on Assets (ROA)

Net Income / Total Assets

Efficiency in using assets

By becoming familiar with these financial statements, you empower yourself to take control of your business’s financial future. Make it a habit to review these statements regularly, and don’t hesitate to seek help from a professional if needed. An informed business owner is a successful business owner!

Spotting Red Flags: Common Bookkeeping Mistakes to Avoid

When managing your small business finances, it’s essential to keep an eye out for common bookkeeping blunders that can lead to bigger financial headaches down the road. Here are some prevalent pitfalls to watch out for:

Neglecting Receipts: Failing to keep track of receipts can lead to missing deductions, ultimately costing you money. Make it a habit to organize and store every receipt digitally or physically as soon as you receive them.

Mixing Personal and Business Finances: This can create chaos in your accounting. Always keep separate bank accounts and credit cards for personal and business transactions to ensure clarity and accuracy.

Inconsistent Bookkeeping: Regularly updating your books is crucial. Establish a routine—whether it’s daily, weekly, or monthly—to ensure your financial records are current and reflect your business’s financial health.

Ignoring Software Tools: Utilizing accounting software can simplify your bookkeeping processes. Don’t shy away from technology; embrace tools that can automate repetitive tasks and reduce the likelihood of human error.

Additionally, some more advanced mistakes can creep up if you’re not careful:

Overlooking Tax Implications: Understanding your tax obligations is crucial. Failing to account for sales tax or payroll taxes can lead to hefty penalties. Regular consultations with a tax professional can help you stay compliant.

Waiting too Long to Reconcile: Reconciling accounts should never be an afterthought. Regular reconciliation can prevent discrepancies that may become problematic if left unchecked for too long.

Not Having a Backup: Whether it’s digital or hard copies, always have a backup of your financial data. This will save you from potential disasters in case of data loss.

To further illustrate the importance of avoiding these mistakes, consider looking at the following table, which outlines the potential repercussions of neglecting proper bookkeeping:

Error

Consequence

Neglecting Receipts

Missed deductions, higher tax liabilities

Mixing Finances

Confusion in reporting, potential legal issues

Inconsistent Records

Inaccurate financial picture, cash flow issues

Ignoring Software

Increased manual errors, wasted time

by being aware of these common mistakes and implementing strategies to avoid them, you can streamline your bookkeeping process and enhance your business’s financial management. Keep your business on the right track by being proactive about your financial health!

The Benefits of Regular Bookkeeping Reviews: Keeping Your Business on Track

Regular bookkeeping reviews serve as a vital compass for your small business, helping you navigate through the complexities of financial management. By consistently evaluating your financial records, you can uncover insights that might otherwise remain obscured. These reviews not only enhance your understanding of your business’s health but also pave the way for more strategic decision-making.

Improved Financial Accuracy: One of the most immediate benefits of frequent bookkeeping reviews is the increased accuracy of your financial records. Regular checks help identify and rectify discrepancies before they escalate into larger issues. This accuracy is crucial for:

Ensuring compliance with tax regulations

Providing trustworthy financial statements to stakeholders

Facilitating smoother audits

Identifying Trends and Patterns: Regular reviews can reveal financial trends that can guide your business strategy. By analyzing your revenue, expenses, and cash flow regularly, you can identify:

Seasonal fluctuations in sales

Cost-cutting opportunities

Product lines that are underperforming

Enhanced Budgeting and Forecasting: Frequent bookkeeping reviews make budgeting and forecasting much more effective. With accurate and updated financial data at your fingertips, you can create budgets that reflect your business’s current situation and future aspirations. This leads to:

Better allocation of resources

More reliable forecasts for cash flow and profits

Informed investment decisions

Boosting Accountability: Regular reviews foster a culture of accountability within your business. When financial records are consistently reviewed, it encourages team members to take ownership of their roles in the financial processes. This accountability leads to:

Increased attention to detail

Proactive problem-solving

Greater overall efficiency

Benefit

Impact on Business

Improved Financial Accuracy

Minimized errors and compliance risks

Identifying Trends

Informed strategic decisions

Enhanced Budgeting

Optimized resource allocation

Boosting Accountability

Improved operational efficiency

the value of regular bookkeeping reviews cannot be overstated. They serve as a backbone for your financial health, revealing insights that empower better decision-making and strategic planning. By committing to this practice, you not only safeguard your business’s future but also position it for sustainable growth and success.

Leveraging Bookkeeping for Business Growth: Insights and Strategies

Effective bookkeeping is not just about tracking your finances; it’s a powerful tool that can drive your business growth. By gaining a thorough understanding of your financial status, you can make informed decisions that lead to sustainable success. Here’s how to leverage your bookkeeping practices to foster growth.

Identify Trends and Patterns

A well-maintained bookkeeping system allows you to analyze historical data, helping you identify trends in revenue, expenses, and customer behavior. Understanding these patterns enables you to:

Anticipate seasonal fluctuations in cash flow.

Adjust your budgeting and financial planning accordingly.

Spot opportunities for cost-saving by analyzing expense trends.

Enhance Financial Visibility

Regular bookkeeping offers a clear picture of your business’s financial health. This transparency is crucial when seeking funding or partnerships. Investors and lenders want to see:

Consistent revenue streams.

Effective expense management.

Accurate forecasts based on solid data.

By presenting these insights, you enhance your credibility and attract potential investors with clear evidence of your business’s financial potential.

Streamline Operations with Technology

Investing in bookkeeping software can revolutionize how you manage your finances. Automation tools can help you:

Reduce manual errors.

Save time through automated invoicing and expense tracking.

Utilizing technology not only enhances accuracy but also frees up your time to focus on core business activities that drive growth.

Make Data-Driven Decisions

Business growth thrives on informed decision-making. With accurate financial data at your fingertips, you can:

Evaluate the profitability of products or services.

Analyze spending to identify areas deserving of investment.

Decide when to scale your operations based on cash flow predictions.

Data-driven decisions reduce risks and enhance the chances of successful outcomes.

Emphasize Strategic Budgeting

Budgeting is more than just a financial exercise; it’s a strategic tool for growth. A robust budget allows you to:

Allocate resources effectively.

Set realistic financial goals.

Monitor performance against budgeted targets.

By aligning your budget with your business growth objectives, you create a roadmap that guides your financial decisions and actions.

Strategy

Benefit

Identifying Trends

Informed decision-making

Enhancing Visibility

Attracting investors

Utilizing Technology

Increased efficiency

Data-Driven Decisions

Reduced risks

Strategic Budgeting

Resource allocation

By implementing these strategies, you can transform your bookkeeping practices into a powerful engine for business growth. It’s not just about keeping the books—it’s about unlocking the potential of your business through informed and strategic financial management.

Conclusion: Taking Control of Your Business Finances for Future Success

In the world of small business, understanding and managing your finances is not just a necessity; it’s a pathway to success. With the right bookkeeping practices in place, you can gain insights into your business operations, allowing for informed decisions that can drive growth and profitability.

Here are a few key strategies to help you take control of your business finances:

Embrace Technology: Utilize accounting software that suits your business needs. Tools like QuickBooks or Xero can automate tasks, track expenses, and generate reports, making your life easier.

Stay Organized: Keep your financial documents in order. Create a digital filing system for invoices, receipts, and statements to access information quickly when needed.

Regularly Review Financial Statements: Make it a habit to check your profit and loss statements, balance sheets, and cash flow reports monthly. This will help you identify trends and make adjustments proactively.

Set a Budget: Develop a realistic budget based on past performance and future forecasts. This will not only guide your spending but also help you plan for unexpected expenses.

Additionally, consider the role of a qualified bookkeeper or accountant in your business. Having a professional can not only minimize errors but also provide valuable insights and advice that can help steer your business in the right direction. They can assist with tax planning, ensuring you’re not leaving money on the table during tax season.

Understanding cash flow is essential: Knowing when money is coming in and going out is vital for maintaining liquidity. You can create a simple cash flow forecast table to visualize your expected inflows and outflows over the coming weeks or months.

Month

Expected Inflows

Expected Outflows

Net Cash Flow

January

$10,000

$8,000

$2,000

February

$12,000

$9,500

$2,500

March

$15,000

$11,000

$4,000

By having a clear view of your cash flow, you can make better decisions about when to invest in new opportunities or when to tighten your belt. This proactive approach will not only help stabilize your finances but also prepare you for future growth.

Lastly, remember that financial literacy is a journey. Continually educate yourself about best practices in bookkeeping and stay updated on financial trends relevant to your industry. Join webinars, read books, and network with fellow business owners to exchange ideas and strategies.

Taking control of your business finances doesn’t happen overnight, but with commitment and the right tools, you’ll be setting yourself up for a successful future. By implementing these practices, you’ll build a solid financial foundation, enabling you to focus on what you do best: growing your business.

Q: Why is bookkeeping important for small businesses?

A: Great question! Bookkeeping is like the backbone of your business. It helps you keep track of every dollar that comes in and goes out. Without accurate records, you can’t make informed decisions, prepare for tax season, or understand your business’s financial health. Think of it this way: good bookkeeping helps you see the bigger picture, so you can steer your business in the right direction.

Q: What are the basic elements of bookkeeping that every small business owner should know?

A: There are a few key elements every small business owner should grasp. First, you need to understand income tracking—this means recording all the money you earn. Second, expense tracking is crucial; you need to know where your money is going. Third, familiarize yourself with your balance sheet and profit and loss statements. These will give you insights into your business’s performance. And remember, consistency is key! Regularly updating your books will save you headaches down the line.

Q: Can I handle bookkeeping myself, or should I hire a professional?

A: It really depends on your comfort level and the complexity of your finances. If you’re just starting and have a simple business model, you might be able to manage your bookkeeping with some software and a bit of learning. However, as your business grows, or if you find finances daunting, hiring a professional can be a game-changer. They can save you time and help you avoid costly mistakes. Plus, having an expert on hand can give you peace of mind!

Q: What software tools are best for small business bookkeeping?

A: There are several fantastic tools out there! QuickBooks is a popular choice for many small businesses due to its user-friendly interface and comprehensive features. FreshBooks is another great option, especially for service-based businesses. If you’re looking for something budget-friendly, Wave offers free accounting software that’s perfect for startups. Do your research and pick a tool that fits your business needs and your level of comfort with technology.

Q: How often should I update my bookkeeping records?

A: Ideally, you should update your records daily or weekly. This might sound like a lot, but it helps keep everything organized and up-to-date. If you wait until the end of the month or worse, the end of the year, you might find it overwhelming—and mistakes can happen. Setting aside a little time each week to tackle your bookkeeping can save you a lot of stress in the long run!

Q: What are some common bookkeeping mistakes to avoid?

A: One of the biggest mistakes is mixing personal and business finances. Keep separate accounts to avoid confusion and complications come tax time. Another common pitfall is neglecting to keep receipts. Always document your expenses! Lastly, failing to reconcile your bank statements regularly can lead to errors going unnoticed. Staying organized and proactive will help you dodge these issues.

Q: How can good bookkeeping contribute to the growth of my business?

A: Good bookkeeping provides clarity and insight into your business’s financial health, which is crucial for growth. With accurate records, you can identify trends, monitor cash flow, and make informed decisions about investments or spending. Additionally, potential investors or lenders will expect to see organized financial records when considering funding your business. So, good bookkeeping isn’t just about keeping the books—it’s about setting your business up for success!

Q: What’s the first step I should take if I want to get my bookkeeping in order?

A: Start by organizing your financial documents. Gather all your receipts, invoices, and bank statements. Next, choose a bookkeeping method—whether that’s manual, software, or hiring a pro. Set up a consistent schedule for updating your records, and make it a non-negotiable part of your week. Remember, the sooner you take action, the easier it will be to get your finances on track and focus on growing your business!

Closing Thoughts:

Bookkeeping may not be the most glamorous part of running a small business, but it’s definitely one of the most important. With the right tools, knowledge, and a bit of discipline, you can turn your bookkeeping into a powerful asset for your business. So, why wait? Start today and watch your business thrive!

The Way Forward

As we wrap up this essential guide to small business bookkeeping, let’s take a moment to reflect on just how critical proper financial management is for your business’s success. We’ve covered the key concepts, tools, and best practices that can transform bookkeeping from a daunting task into a seamless part of your daily operations.

Remember, keeping your books in order isn’t just about taxes and compliance; it’s about gaining insights into your business’s health and making informed decisions that can propel you forward. Whether you’re just starting out or looking to refine your existing processes, the right bookkeeping practices can save you time, reduce stress, and ultimately boost your bottom line.

So, why not take that first step today? Invest a little time in your financial foundation, and watch how it pays off in the long run. If you need support, consider reaching out to a professional or utilizing some of the fantastic software options available. Your future self—and your business—will thank you for it!

Now go ahead and tackle those numbers with confidence. You’ve got this!